Comparison of Estimators#

MMSE estimator

MAP estimator

ML estimator

Summary of Previous Results#

Problem Statement

In this example, based on [B2, Ex 10.7], we want to find the estimate \(\hat{\boldsymbol{\mu}}\) of the unknown random mean \(\boldsymbol{\mu}\), using the set of observations \(\mathbf{y}_1, \ldots, \mathbf{y}_m\).

Assume further that the observations are statistically independent, normal random variables, each with unknown mean \(\boldsymbol{\mu}\) and known variance \(\sigma^2\).

The conditional pdf \(p(\vec{y}|\mu)\) is then

Next, assume that the a priori pdf \(p(\mu)\) is normal with mean \(m_1\) and variance \(\beta^2\), i.e.,

Note that the prior \( p(\mu) \) represents our knowledge about \(\mu\) before observing any data.

The MMSE, MAP, and ML estimates are, respectively:

Comparison of Estimators of Parameters

The first two estimates, \(\hat{\boldsymbol{\mu}}_{\text{MMSE}}\) and \(\hat{\boldsymbol{\mu}}_{\text{MAP}}\), are described as identical and biased.

The third estimate, \(\hat{\boldsymbol{\mu}}_{\text{ML}}\), is unbiased and efficient.

For large sample sizes \( m \) or large \( \beta^2 \), it is noted that \( \hat{\boldsymbol{\mu}}_{\text{MMSE}} (= \hat{\boldsymbol{\mu}}_{\text{MAP}}) \approx \bar{\mathbf{y}} = \hat{\boldsymbol{\mu}}_{\text{ML}} \) are approximately equal.

Large \( \beta^2 \) corresponds to an a priori probability density function (pdf) with a wide dispersion, meaning that little statistical information is gained from the prior knowledge.

In this case, the MMSE and MAP estimates reduce to the ML estimate, which does not require an a priori pdf.

import numpy as np

import matplotlib.pyplot as plt

import pandas as pd

# Set random seed for reproducibility (optional)

# np.random.seed(42)

# Parameters

m1 = 0.0 # Prior mean of mu

beta = 1.0 # Prior standard deviation of mu

sigma = 1.0 # Known standard deviation of observations

m = 10 # Number of observations per trial

k = 5 # Number of trials

# To store results

results = {

'Trial': [],

'True_mu': [],

'Observations': [],

'Sample_mean_y_bar': [],

'MLE': [],

'MAP': [],

'MMSE': []

}

for trial in range(1, k + 1):

# 1. Generate true mu based on prior

true_mu = np.random.normal(m1, beta)

# 2. Generate observations based on true mu

observations = np.random.normal(true_mu, sigma, m)

y_bar = np.mean(observations)

# 3. Compute estimates

# MLE: Sample mean

mle = y_bar

# MAP: (beta^2 * y_bar + sigma^2 * m1) / (beta^2 + sigma^2)

map_estimate = (beta**2 * y_bar + sigma**2 * m1) / (beta**2 + sigma**2)

# MMSE: Same as MAP in Gaussian case

mmse = map_estimate

# 4. Store the results

results['Trial'].append(trial)

results['True_mu'].append(true_mu)

results['Observations'].append(observations)

results['Sample_mean_y_bar'].append(y_bar)

results['MLE'].append(mle)

results['MAP'].append(map_estimate)

results['MMSE'].append(mmse)

# 5. Print the results for the current trial

observations_str = np.array2string(observations, precision=4, separator=', ', suppress_small=True)

print(f"Trial {trial}:")

print(f"True μ: {true_mu:.4f}")

print(f"Observations (vector y): {observations_str}")

print(f"Statistic (sample mean ȳ): {y_bar:.4f}")

print(f"MLE Estimate: {mle:.4f}")

print(f"MAP Estimate: {map_estimate:.4f}")

print(f"MMSE Estimate: {mmse:.4f}\n")

# Convert results to a DataFrame for better visualization

# Since 'Observations' is an array, we'll keep it as is or process separately if needed

df_results = pd.DataFrame({

'Trial': results['Trial'],

'True_mu': results['True_mu'],

'Sample_mean_y_bar': results['Sample_mean_y_bar'],

'MLE': results['MLE'],

'MAP': results['MAP'],

'MMSE': results['MMSE']

})

# Display the results table

print("Summary of Results:")

print(df_results.to_string(index=False))

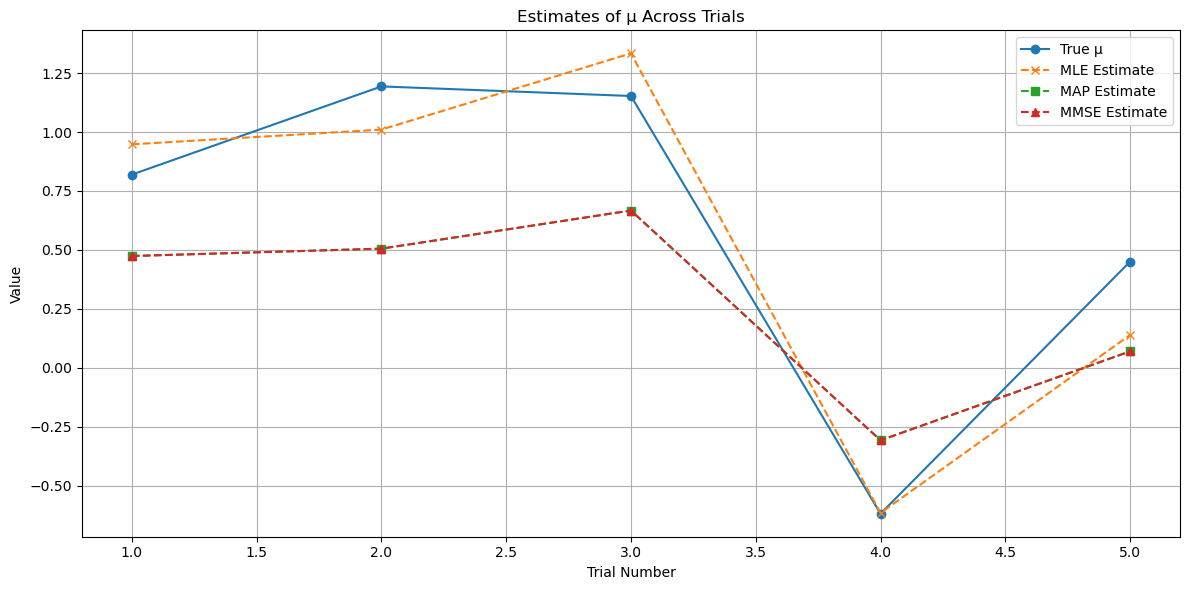

# Visualization: Compare estimates with true mu across trials

plt.figure(figsize=(12, 6))

plt.plot(df_results['Trial'], df_results['True_mu'], marker='o', label='True μ')

plt.plot(df_results['Trial'], df_results['MLE'], marker='x', linestyle='--', label='MLE Estimate')

plt.plot(df_results['Trial'], df_results['MAP'], marker='s', linestyle='--', label='MAP Estimate')

plt.plot(df_results['Trial'], df_results['MMSE'], marker='^', linestyle='--', label='MMSE Estimate')

plt.title('Estimates of μ Across Trials')

plt.xlabel('Trial Number')

plt.ylabel('Value')

plt.legend()

plt.grid(True)

plt.tight_layout()

plt.show()

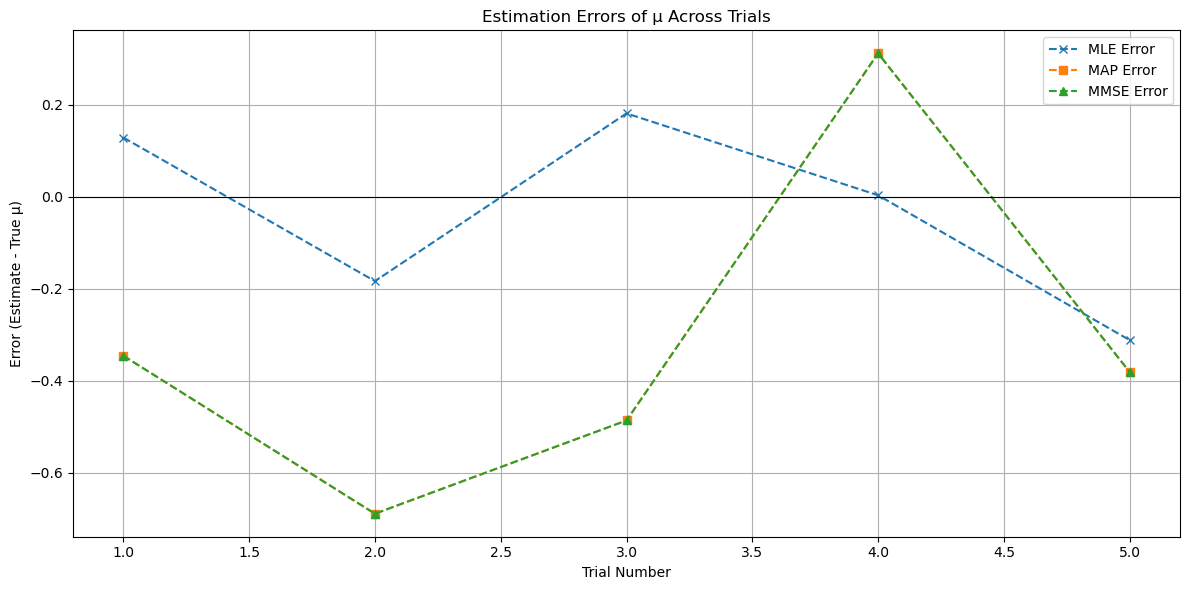

# Optional: Compute and display estimation errors

df_results['MLE_Error'] = df_results['MLE'] - df_results['True_mu']

df_results['MAP_Error'] = df_results['MAP'] - df_results['True_mu']

df_results['MMSE_Error'] = df_results['MMSE'] - df_results['True_mu']

print("\nEstimation Errors:")

print(df_results[['Trial', 'MLE_Error', 'MAP_Error', 'MMSE_Error']].to_string(index=False))

# Optional: Plot estimation errors

plt.figure(figsize=(12, 6))

plt.plot(df_results['Trial'], df_results['MLE_Error'], marker='x', linestyle='--', label='MLE Error')

plt.plot(df_results['Trial'], df_results['MAP_Error'], marker='s', linestyle='--', label='MAP Error')

plt.plot(df_results['Trial'], df_results['MMSE_Error'], marker='^', linestyle='--', label='MMSE Error')

plt.axhline(0, color='black', linewidth=0.8)

plt.title('Estimation Errors of μ Across Trials')

plt.xlabel('Trial Number')

plt.ylabel('Error (Estimate - True μ)')

plt.legend()

plt.grid(True)

plt.tight_layout()

plt.show()

Trial 1:

True μ: 0.8193

Observations (vector y): [ 2.1743, 0.905 , 1.6846, 0.0631, 1.1597, 1.6086, 2.9175, -0.4643,

-0.7197, 0.1486]

Statistic (sample mean ȳ): 0.9477

MLE Estimate: 0.9477

MAP Estimate: 0.4739

MMSE Estimate: 0.4739

Trial 2:

True μ: 1.1935

Observations (vector y): [-0.379 , 3.1874, -0.6197, 1.6783, 0.7355, -0.5886, 2.1176, 1.289 ,

0.8837, 1.7972]

Statistic (sample mean ȳ): 1.0101

MLE Estimate: 1.0101

MAP Estimate: 0.5051

MMSE Estimate: 0.5051

Trial 3:

True μ: 1.1528

Observations (vector y): [ 2.6225, 0.9805, -0.1892, 2.4647, 0.8227, 1.5908, 0.3552, 2.4536,

1.2346, 1.0021]

Statistic (sample mean ȳ): 1.3337

MLE Estimate: 1.3337

MAP Estimate: 0.6669

MMSE Estimate: 0.6669

Trial 4:

True μ: -0.6195

Observations (vector y): [-0.7227, -0.795 , -1.567 , -1.3811, -1.4331, -2.0088, 0.9924, 1.7117,

1.1856, -2.1459]

Statistic (sample mean ȳ): -0.6164

MLE Estimate: -0.6164

MAP Estimate: -0.3082

MMSE Estimate: -0.3082

Trial 5:

True μ: 0.4501

Observations (vector y): [ 2.5458, 0.4679, 1.1959, -1.2552, -1.0884, -0.1493, -1.6052, -1.8537,

2.4189, 0.7099]

Statistic (sample mean ȳ): 0.1387

MLE Estimate: 0.1387

MAP Estimate: 0.0693

MMSE Estimate: 0.0693

Summary of Results:

Trial True_mu Sample_mean_y_bar MLE MAP MMSE

1 0.819300 0.947741 0.947741 0.473871 0.473871

2 1.193471 1.010134 1.010134 0.505067 0.505067

3 1.152803 1.333739 1.333739 0.666869 0.666869

4 -0.619528 -0.616388 -0.616388 -0.308194 -0.308194

5 0.450150 0.138650 0.138650 0.069325 0.069325

Estimation Errors:

Trial MLE_Error MAP_Error MMSE_Error

1 0.128441 -0.345429 -0.345429

2 -0.183338 -0.688404 -0.688404

3 0.180936 -0.485934 -0.485934

4 0.003140 0.311334 0.311334

5 -0.311499 -0.380825 -0.380825

Example: Signal Reception in Noise#

In this example, based on [B2, Ex 10.20], we consider the reception of a signal embedded in noise, a common scenario in communications theory.

Problem Statement

We have \( L \) independent observations (or received-signal samples) \( \mathbf{y}_i \), which are expressed as the sum of a random signal \( \mathbf{s} \) and noise samples \( \mathbf{n}_i \):

Assumptions and PDFs

The random signal \( \mathbf{s} \) is uniformly distributed in the interval \( (0, a) \).

The pdf of the signal \( s \) is given by:

The random noise \( \mathbf{n}_i \) is Gaussian with zero mean and variance \( \sigma^2 \).

The pdf of the noise \( \mathbf{n}_i \) is:

Conditional Distribution of \( \mathbf{y}_i \) given \( s \)

For a constant \( s \), \( \mathbf{y}_i \) is Gaussian with mean \( s \) and variance \( \sigma^2 \).

Thus, the pdf \( p(\vec{y} | s) \) can be written as:

Task

We want to estimate the random \(\mathbf{s}\).

import numpy as np

import matplotlib.pyplot as plt

# Parameters

a = 1 # Upper bound for the true signal

sigma = 1 # Standard deviation of the noise

L = 10 # Number of observations per trial

k = 5 # Number of trials

# To store signals and observations for analysis

signals = []

observations = []

for trial in range(1, k + 1):

# Generate a random true signal within (0, a)

signal = np.random.uniform(0, a)

# Generate Gaussian noise

noise = np.random.normal(0, sigma, L)

# Generate observations by adding noise to the signal

y = signal + noise

# Store the results

signals.append(signal)

observations.append(y)

# Display the results for the current trial

print(f"Trial {trial}:")

print(f"True Signal (fixed parameter s): {signal:.4f}")

print(f"Observations (vector y): {y}\n")

Trial 1:

True Signal (fixed parameter s): 0.4516

Observations (vector y): [ 1.32064602 -0.5077289 -0.66214343 1.44271647 -0.82477021 1.81397064

-0.80037337 -0.19763709 0.37709459 0.27959563]

Trial 2:

True Signal (fixed parameter s): 0.2683

Observations (vector y): [-0.52152635 0.38722607 0.35052791 1.02839825 1.951469 -0.62050193

0.63186598 -0.77860689 1.50367162 -0.24161981]

Trial 3:

True Signal (fixed parameter s): 0.1999

Observations (vector y): [ 1.43114502 -1.42366952 -0.05386208 0.39046 0.04691115 1.44249959

-1.57316783 0.05206321 0.56235636 0.17916296]

Trial 4:

True Signal (fixed parameter s): 0.3236

Observations (vector y): [-1.7656375 1.89771449 -0.05695857 0.94111807 2.5332734 -0.54548923

-0.80319628 -0.61812149 0.46580735 -0.09023442]

Trial 5:

True Signal (fixed parameter s): 0.0654

Observations (vector y): [ 0.00732296 0.30873143 -1.37173128 1.80500289 -0.22437932 -0.70756438

0.8684864 1.24873887 0.26297671 1.87421202]

Method 1: Maximum Likelihood Estimate#

Recall that the Maximum Likelihood Estimator seeks the value of \( s \) that maximizes the likelihood of the observed data \( \vec{y} = (y_1, y_2, \dots, y_L) \).

Mathematically, the ML estimator is given by:

Unlike MAP estimation, ML does not consider the prior distribution \( p(s) \).

Finding \( \hat{s}_{\text{ML}} \)#

We need to maximize the likelihood \( p(\vec{y} | s) \) with respect to \( s \).

Maximizing the likelihood is equivalent to maximizing the log-likelihood since the logarithm is a monotonically increasing function.

The log-likelihood \( \mathcal{L}(s) \) is:

To maximize \( \mathcal{L}(s) \), we can equivalently minimize the negative log-likelihood:

This is a quadratic function in \( s \), which is minimized when its derivative with respect to \( s \) is zero.

Compute the derivative of the sum of squared errors with respect to \( s \):

Set the derivative to zero for minimization:

Simplifying:

where \( \bar{y} \) is the sample mean of the observations.

The Maximum Likelihood Estimator for \( s \) is the sample mean of the observations:

In general

where \( \bar{\mathbf{y}} \) is the sample mean.

Note that, unless explicitly stated, ML estimation typically assumes an unconstrained parameter space.

Method 2: Maximum A Posteriori Estimate (MAP)#

The MAP estimator seeks the value of \( s \) that maximizes the posterior distribution \( p(s | \vec{y}) \), where \( \vec{y} = (y_1, y_2, \dots, y_L) \) represents all observations.

Mathematically, the MAP estimator is given by:

By Bayes’ theorem:

Since \( p(\vec{y}) \) is constant with respect to \( s \), maximizing \( p(s | \vec{y}) \) is equivalent to maximizing the product of the likelihood \( p(\vec{y} | s) \) and the prior \( p(s) \):

Combining the likelihood and the prior, the MAP estimator maximizes:

Substituting the expressions:

Since \( \left( \frac{1}{\sqrt{2\pi \sigma^2}} \right)^L \) and \( \frac{1}{a} \) are constants (when \( 0 < s < a \)), maximizing the above expression reduces to minimizing the exponent term within the allowed range of \( s \):

Solving the differential equation#

The expression to minimize is a quadratic function in \( s \):

Taking the derivative with respect to \( s \) and setting it to zero to find the minimum:

Solving for \( s \):

where \( \bar{y} \) is the sample mean of the observations.

The MAP estimator must respect the prior constraints \( 0 < s < a \). Therefore, the estimator is:

This can be compactly written using the clipping (or saturation) function:

Putting it all together, the MAP estimator for \( s \) is:

Method 3: Minimum Mean Squared Error (MMSE) Estimate#

Problem Formulation#

The MMSE Estimator seeks to minimize the mean squared error between the estimated signal \( \hat{s} \) and the true signal \( s \). Mathematically, it is defined as:

Using Bayesian estimation, this expectation can be expressed as:

Substituting the expressions for \( p(\vec{y}|s) \) and \( p(s) \) into the MMSE formula:

Given the support of \( p(s) \) is \( (0, a) \), the integrals simplify to:

Since \( \frac{1}{a} \) is a constant, it cancels out in the numerator and denominator:

Notice that:

where \( \bar{y} = \frac{1}{L} \sum_{i=1}^{L} y_i \) is the sample mean.

Thus, the joint likelihood becomes:

The term \( \sum_{i=1}^{L} (y_i - \bar{y})^2 \) is independent of \( s \), so it acts as a constant in both the numerator and denominator and cancels out. Therefore:

Derivation of the MMSE Estimate#

To evaluate the integrals, perform a change of variables to standardize the Gaussian exponent.

Let:

Thus:

Constraints from the prior probability \(p(s)\):

When \( s = 0 \):

\[ z_1 = \frac{ 0 - \bar{y} }{ \tau } = -\frac{ \bar{y} \sqrt{L} }{ \sigma } \]When \( s = a \):

\[ z_2 = \frac{ a - \bar{y} }{ \tau } = \frac{ (a - \bar{y}) \sqrt{L} }{ \sigma } \]

Substituting into the integrals:

Simplifying, the \( \tau \) terms cancel out:

Split the numerator:

For the first integral

where \( \Phi(z) \) is the standard normal cumulative distribution function (CDF), i.e., \(\Phi(z) = 1- Q(z)\).

For the second integral

Thus, the numerator becomes:

And the denominator is:

Therefore, the MMSE estimator is:

Recall that:

Substituting these back:

Simplifying:

Note: \( \Phi(-x) = 1 - \Phi(x) \), so:

Thus, the denominator can be rewritten as:

Therefore, the MMSE estimator simplifies to:

Alternatively, using the error function \( \text{erf}(x) \), which is related to the standard normal CDF \( \Phi(x) \) by:

We can express the MMSE estimator as:

Simplifying the denominator:

Thus, the MMSE estimator becomes:

This expression neatly encapsulates the MMSE estimator in terms of the sample mean \( \bar{y} \), the error function, and the system parameters \( a \), \( \sigma \), and \( L \).

Summary: Expressions for the MMSE Estimator

To present the MMSE estimator in a compact and interpretable form, we can express it as:

Alternatively, using the error function \( \text{erf}(x) \):

where

\( \bar{y} = \frac{1}{L} \sum_{i=1}^{L} y_i \) is the sample mean.

\( \Phi(x) \) is the standard normal CDF.

\( \text{erf}(x) \) is the error function, related to the standard normal CDF by:

\[ \Phi(x) = \frac{1}{2} \left[ 1 + \text{erf}\left( \frac{x}{\sqrt{2}} \right) \right] \]

Example Calculation#

Given:

\( L = 10 \) observations:

\[ \vec{y} = [2.0, 2.2, 1.8, 2.1, 2.3, 2.0, 2.1, 2.2, 1.9, 2.0] \]\( a = 3 \)

\( \sigma = 0.5 \)

Calculate the Sample Mean:

Compute the MMSE Estimator:

Substitute the values into the MMSE estimator formula:

Calculating each component:

Exponentials

CDFs

Thus:

Substituting Back

Thus, we have

Since the sample mean \( \bar{y} = 2.06 \) lies well within the interval \( (0, 3) \), the MMSE estimator closely aligns (not identical, because this is an approximation) with the sample mean, as expected.

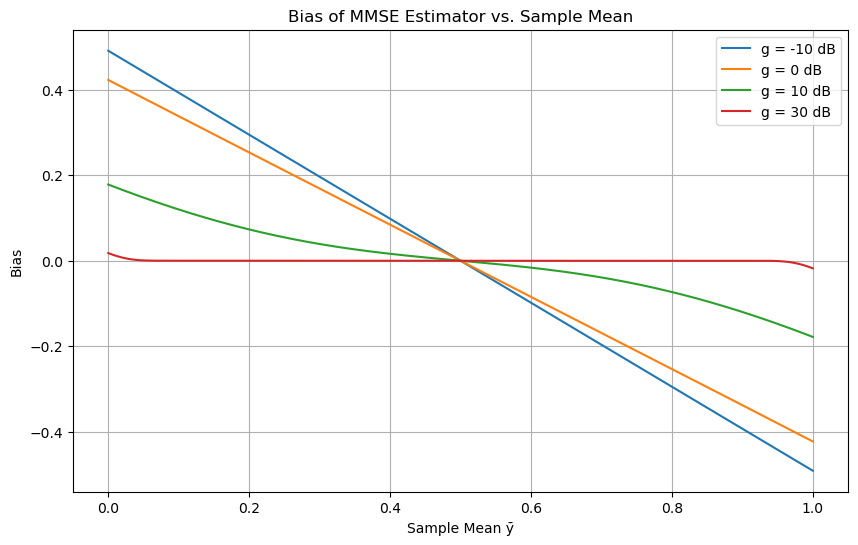

Biasness of MMSE#

Bias: The final expression shows that the MMSE estimate \( \hat{s}_{MS} \) is biased. This contrasts with the ML and MAP estimates, which are unbiased.

The bias term (involving \( \bar{y} \)) can be numerically evaluated to show how its bias is affected by a parameter defined in decibels (dB).

The quality of the estimate depends on the parameter \( L / (2\sigma^2) \), which is expressed in decibels as:

The MMSE estimator expressed as a function of \( g = \frac{L}{2\sigma^2} \) (linear) as

import numpy as np

import matplotlib.pyplot as plt

from scipy.special import erf

# Define the MMSE estimator function

def mmse_estimator(y_bar, g, a=1):

numerator = np.exp(-g * y_bar**2) - np.exp(-g * (a - y_bar)**2)

denominator = erf((a - y_bar) * np.sqrt(g)) + erf(y_bar * np.sqrt(g))

# To handle division by zero, we add a small epsilon to the denominator

epsilon = 1e-12

denominator = np.where(denominator == 0, epsilon, denominator)

estimator = y_bar + (1 / np.sqrt(np.pi * g)) * (numerator / denominator)

return estimator

# Parameters

a = 1

y_bar = np.linspace(0, a, 1000)

g_dB_values = [-10, 0, 10, 30]

g_values = 10 ** (np.array(g_dB_values) / 10)

# Plotting

plt.figure(figsize=(10, 6))

for g_dB, g in zip(g_dB_values, g_values):

estimator = mmse_estimator(y_bar, g, a)

bias = estimator - y_bar

plt.plot(y_bar, bias, label=f'g = {g_dB} dB')

plt.title('Bias of MMSE Estimator vs. Sample Mean')

plt.xlabel('Sample Mean ȳ')

plt.ylabel('Bias')

plt.legend()

plt.grid(True)

plt.show()

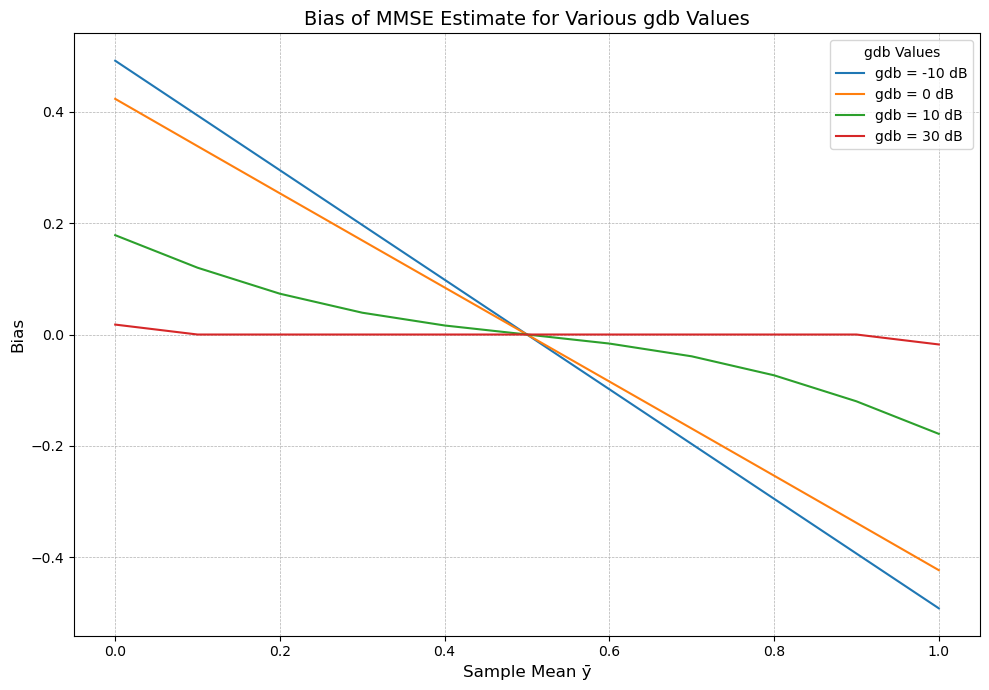

Schonhoff’s Method#

import numpy as np

import matplotlib.pyplot as plt

from scipy.stats import norm

def bias(gdb):

"""

Calculate the bias of the MMSE Estimate for a given gdb.

Parameters:

gdb (float): g in decibels, defined as 10 * log10(L / (2 * sigma^2))

Returns:

b (numpy.ndarray): Bias of the MMSE estimate for y ranging from 0 to 1 in steps of 0.1

"""

# Convert gdb from decibels to linear scale

g = 10**(0.1 * gdb)

# Calculate coefficients

coef = 1 / np.sqrt(np.pi * g)

sig = 1 / np.sqrt(2 * g)

# Initialize bias array

b = np.zeros(11)

# Calculate bias for y values from 0 to 1 in steps of 0.1

for k in range(1, 12):

y = (k - 1) * 0.1

t1 = np.exp(-y**2 * g)

t2 = np.exp(-(y - 1)**2 * g)

if np.isclose(t1, t2):

b[k-1] = 0

else:

td1 = norm.cdf(y, loc=0, scale=sig)

td2 = norm.cdf(y, loc=1, scale=sig)

denominator = 2 * (td1 - td2)

# To avoid division by zero, check if denominator is not zero

if not np.isclose(denominator, 0):

b[k-1] = coef * (t1 - t2) / denominator

else:

b[k-1] = 0 # Assign zero or handle as needed

return b

def plot_bias(gdb_values, y_range=(0, 1), step=0.1):

"""

Plot the bias of the MMSE Estimate for multiple gdb values.

Parameters:

gdb_values (list or array-like): List of gdb values in decibels to plot

y_range (tuple): The range of y values (start, end)

step (float): Step size for y values

"""

# Create y-axis values based on the specified range and step

y_values = np.arange(y_range[0], y_range[1] + step, step)

plt.figure(figsize=(10, 7))

for gdb in gdb_values:

bias_values = bias(gdb)

plt.plot(y_values, bias_values, linestyle='-', label=f'gdb = {gdb} dB')

plt.grid(True, which='both', linestyle='--', linewidth=0.5)

plt.xlabel('Sample Mean ȳ', fontsize=12)

plt.ylabel('Bias', fontsize=12)

plt.title('Bias of MMSE Estimate for Various gdb Values', fontsize=14)

plt.legend(title='gdb Values', fontsize=10)

plt.tight_layout()

plt.show()

# Example usage

if __name__ == "__main__":

# Define multiple gdb values

gdb_values = [-10, 0, 10, 30] # You can add more values as needed

# Plot bias for the specified gdb values

plot_bias(gdb_values)

The bias decreases as \( g_{dB} \) increases, and as \( g_{dB} \) becomes large, the bias term approaches zero, meaning the MMSE estimate becomes closer to unbiased.

We can say that the larger the signal-to-noise ratio (expressed by \( g_{dB} \)), the smaller the bias in the MMSE estimate.

Discussion#

Data Integration: The MMSE estimator \( \hat{s}_{\text{MMSE}} \) integrates both the observed data (through the sample mean \( \bar{y} \)) and the prior information about \( s \) (uniformly distributed over \( (0, a) \)). This ensures that the estimator not only fits the data but also adheres to the known constraints on \( s \).

Bias-Variance Trade-off: Unlike the Maximum Likelihood estimator, which solely relies on data and can be biased when data suggests estimates outside \( (0, a) \), the MMSE estimator incorporates prior knowledge to potentially introduce bias that reduces the overall mean squared error.

Behavior Near Boundaries:

Central Estimates (\( \bar{y} \) well within \( (0, a) \)): The MMSE estimator closely aligns with the sample mean, similar to the ML estimator.

Boundary Estimates (\( \bar{y} \) near 0 or \( a \)): The estimator adjusts the estimate to respect the prior constraints, preventing it from exceeding the bounds. This results in a smoother transition compared to the ML estimator, which might abruptly clip estimates.

Simulation of 3 Methods#

import numpy as np

import matplotlib.pyplot as plt

from scipy.stats import norm

from scipy.integrate import quad

from scipy.special import erf

# Simulation Parameters

L = 10 # Number of observations

a = 3.0 # Upper bound for s

sigma = 2 # Noise standard deviation

num_trials = 1000 # Number of simulation trials

# Function to compute MMSE estimator via numerical integration

def mmse_estimator_numerical(y_bar, L, sigma, a):

# Define the integrand for the numerator: s * exp(- (L/(2*sigma^2)) * (s - y_bar)^2)

def numerator_integrand(s):

return s * np.exp(- (L / (2 * sigma**2)) * (s - y_bar)**2)

# Define the integrand for the denominator: exp(- (L/(2*sigma^2)) * (s - y_bar)^2)

def denominator_integrand(s):

return np.exp(- (L / (2 * sigma**2)) * (s - y_bar)**2)

# Compute the integrals numerically

numerator, _ = quad(numerator_integrand, 0, a, limit=100)

denominator, _ = quad(denominator_integrand, 0, a, limit=100)

# Avoid division by zero

if denominator == 0:

return 0

else:

return numerator / denominator

# Function to compute MMSE estimator via closed-form expression

def mmse_estimator_closed_form(y_bar, L, sigma, a):

# Compute the exponent terms

exponent1 = - (y_bar ** 2) * L / (2 * sigma ** 2)

exponent2 = - ((a - y_bar) ** 2) * L / (2 * sigma ** 2)

# Compute the numerator and denominator

numerator = np.exp(exponent1) - np.exp(exponent2)

# Compute the error functions

erf1 = erf((a - y_bar) * np.sqrt(L) / (sigma * np.sqrt(2)))

erf2 = erf(y_bar * np.sqrt(L) / (sigma * np.sqrt(2)))

# Compute the denominator of the fraction inside the formula

denominator = 0.5 * (erf1 + erf2)

# Avoid division by zero

if denominator == 0:

adjustment = 0

else:

adjustment = (sigma / np.sqrt(2 * np.pi * L)) * (numerator / denominator)

# Compute the closed-form MMSE estimator

s_mmse_closed = y_bar + adjustment

return s_mmse_closed

# Function to compute MAP estimator via theory

def map_estimator_closed_form(y_bar, a):

return min(a, max(0, y_bar))

# Function to compute MAP estimator via numerical root-finding (generalized approach)

def map_estimator_numerical(y_bar, L, sigma, a):

# Define the derivative of log p(s | y) with respect to s

def derivative_log_posterior(s):

# For uniform prior, p(s) is constant within [0, a]

# So derivative is same as derivative of log p(y | s)

# p(y | s) ~ exp(- (sum (y_i - s)^2)/(2 sigma^2))

# derivative: d/ds log p(y | s) = sum (y_i - s) / sigma^2 = L (y_bar - s) / sigma^2

return L * (y_bar - s) / (sigma ** 2)

# Attempt to find the root within [0, a]

# Given the derivative is linear in s, the root is at s = y_bar

# Clamp the root to [0, a]

s_root = y_bar

s_root_clamped = min(a, max(0, s_root))

return s_root_clamped

# Initialize arrays to store results

ml_estimates = np.zeros(num_trials)

map_estimates_closed_form = np.zeros(num_trials)

map_estimates_numerical = np.zeros(num_trials)

mmse_estimates_numerical = np.zeros(num_trials)

mmse_estimates_closed = np.zeros(num_trials)

true_signals = np.zeros(num_trials)

# Simulation Loop

for trial in range(num_trials):

# Randomly choose a true signal s within (0, a)

s = np.random.uniform(0, a)

true_signals[trial] = s

# Generate L observations with Gaussian noise

y = s + np.random.normal(0, sigma, L)

y_bar = np.mean(y)

# ML Estimator

s_ml = y_bar

ml_estimates[trial] = s_ml

# MAP Estimator via Closed-Form

s_map_proj = map_estimator_closed_form(y_bar, a)

map_estimates_closed_form[trial] = s_map_proj

# MAP Estimator via Numerical Root-Finding

s_map_num = map_estimator_numerical(y_bar, L, sigma, a)

map_estimates_numerical[trial] = s_map_num

# MMSE Estimator via Numerical Integration

s_mmse_num = mmse_estimator_numerical(y_bar, L, sigma, a)

mmse_estimates_numerical[trial] = s_mmse_num

# MMSE Estimator via Closed-Form Expression

s_mmse_closed = mmse_estimator_closed_form(y_bar, L, sigma, a)

mmse_estimates_closed[trial] = s_mmse_closed

# Compute Squared Errors

ml_errors = (true_signals - ml_estimates) ** 2

map_errors_proj = (true_signals - map_estimates_closed_form) ** 2

map_errors_num = (true_signals - map_estimates_numerical) ** 2

mmse_errors_num = (true_signals - mmse_estimates_numerical) ** 2

mmse_errors_closed_form = (true_signals - mmse_estimates_closed) ** 2

# Compute Mean Squared Errors

mse_ml = np.mean(ml_errors)

mse_map_proj = np.mean(map_errors_proj)

mse_map_num = np.mean(map_errors_num)

mse_mmse_num = np.mean(mmse_errors_num)

mse_mmse_closed = np.mean(mmse_errors_closed_form)

print(f"Mean Squared Error (ML Estimator): {mse_ml:.5f}")

print(f"Mean Squared Error (MAP Estimator - Closed-Form): {mse_map_proj:.5f}")

print(f"Mean Squared Error (MAP Estimator - Numerical): {mse_map_num:.5f}")

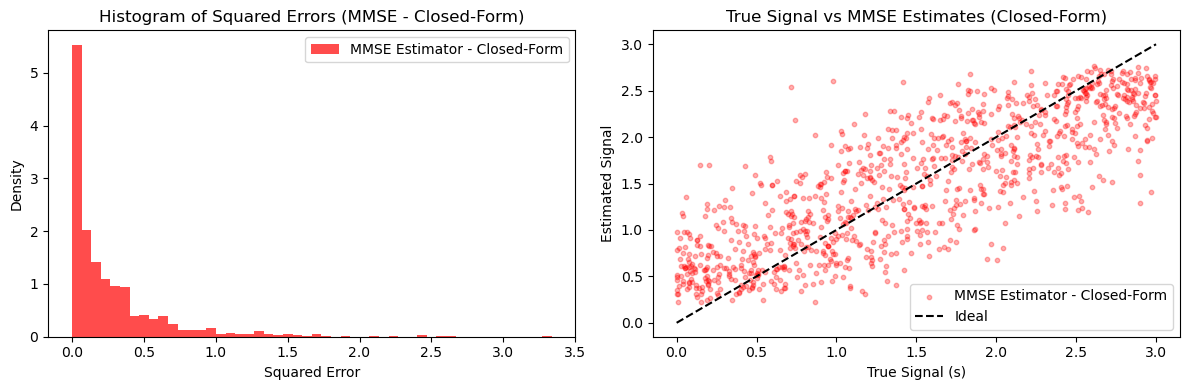

print(f"Mean Squared Error (MMSE Estimator - Closed-Form): {mse_mmse_closed:.5f}")

print(f"Mean Squared Error (MMSE Estimator - Numerical): {mse_mmse_num:.5f}")

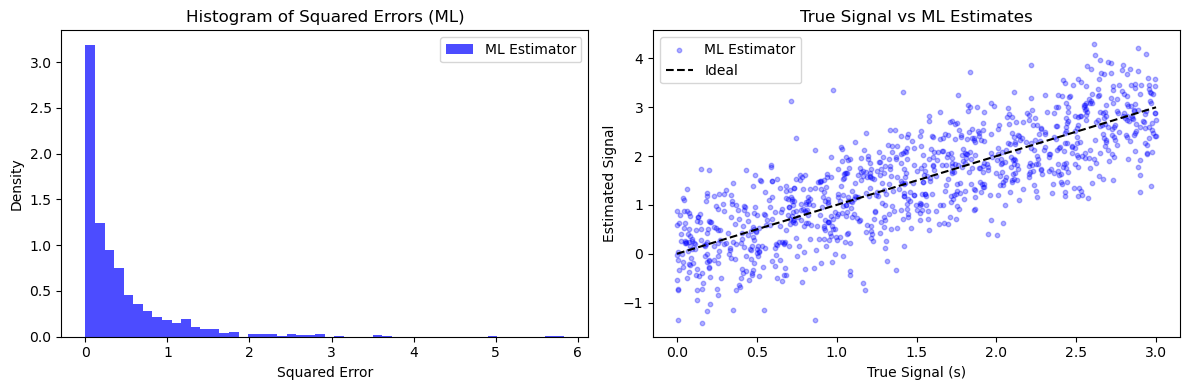

Mean Squared Error (ML Estimator): 0.41932

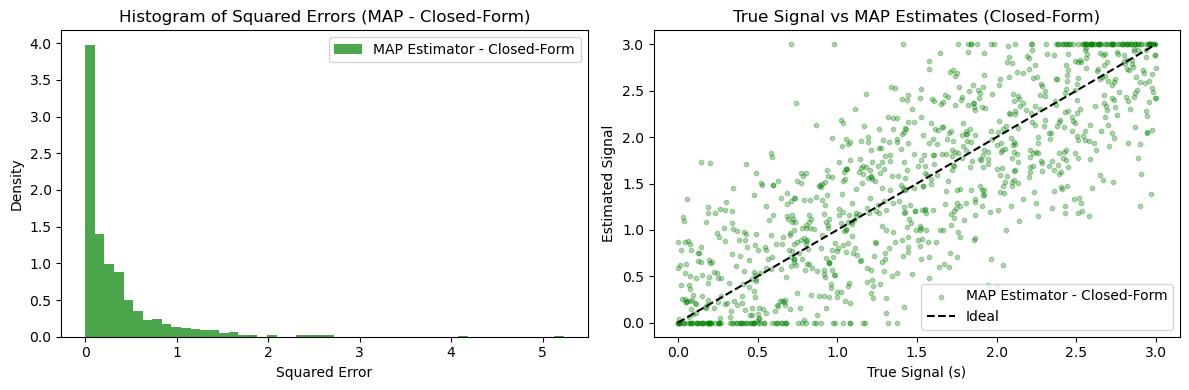

Mean Squared Error (MAP Estimator - Closed-Form): 0.32206

Mean Squared Error (MAP Estimator - Numerical): 0.32206

Mean Squared Error (MMSE Estimator - Closed-Form): 0.26368

Mean Squared Error (MMSE Estimator - Numerical): 0.26368

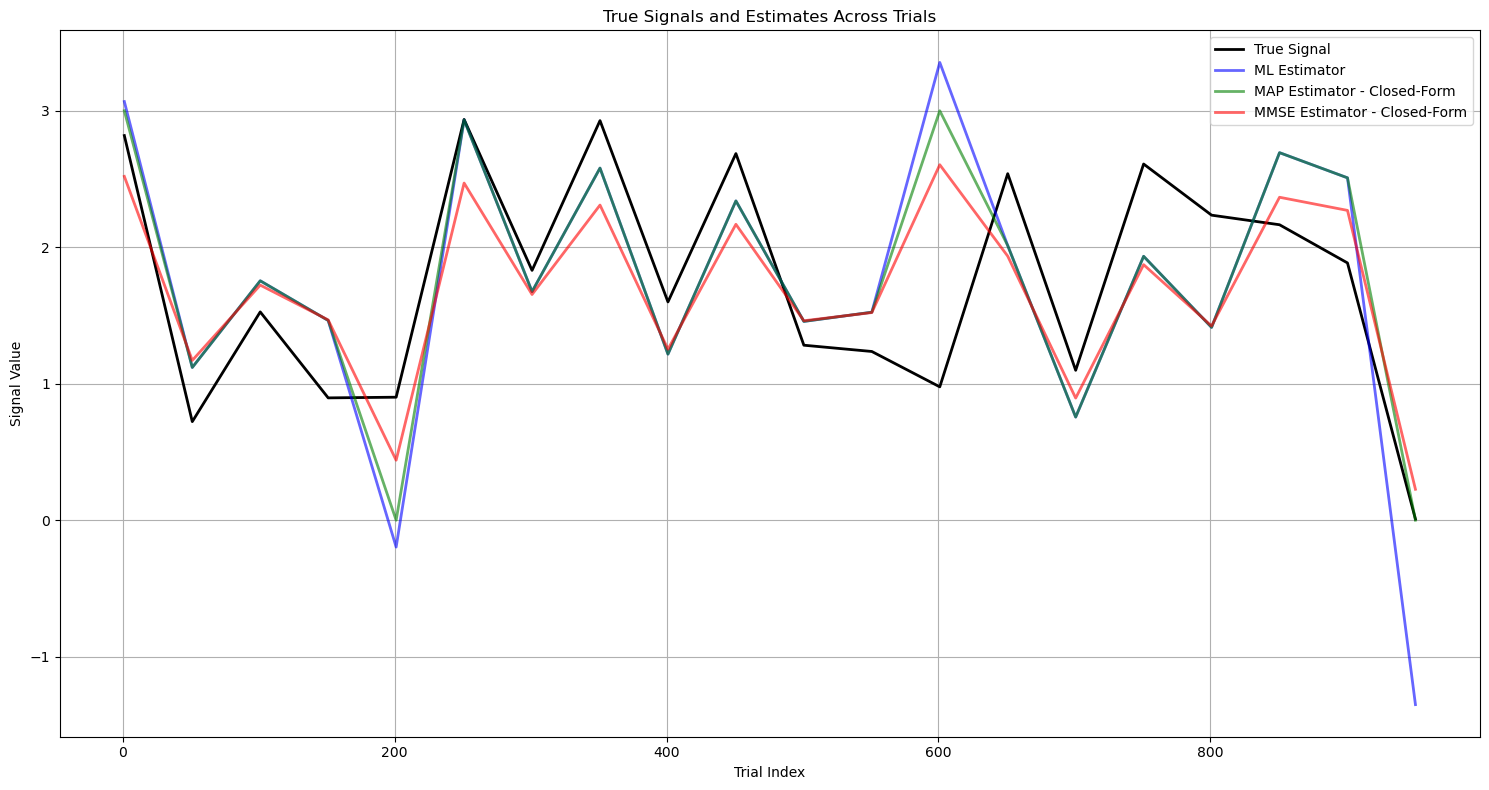

# Additional Plot: True Signals vs Selected Estimators with Trial Index on X-axis

# To visualize how estimates evolve over trials, we can plot the estimators against trial index.

# To make the plot readable, especially with huge trials, we'll plot a subset, e.g., every k-th trial.

subset_indices = np.arange(0, num_trials, 50)

subset_trials = subset_indices + 1 # Trial indices starting from 1

plt.figure(figsize=(15, 8))

plt.plot(subset_trials, true_signals[subset_indices],

label='True Signal', color='black', linewidth=2)

plt.plot(subset_trials, ml_estimates[subset_indices],

label='ML Estimator', color='blue', alpha=0.6, linewidth=2)

plt.plot(subset_trials, map_estimates_closed_form[subset_indices],

label='MAP Estimator - Closed-Form', color='green', alpha=0.6, linewidth=2)

plt.plot(subset_trials, mmse_estimates_closed[subset_indices],

label='MMSE Estimator - Closed-Form', color='red', alpha=0.6, linewidth=2)

plt.title('True Signals and Estimates Across Trials')

plt.xlabel('Trial Index')

plt.ylabel('Signal Value')

plt.legend()

plt.grid(True)

plt.tight_layout()

plt.show()

# Plotting Histograms of Squared Errors and True Signal vs Estimates in pairs

# Pair 1: ML Estimator

plt.figure(figsize=(12, 4))

plt.subplot(1, 2, 1)

plt.hist(ml_errors, bins=50, alpha=0.7, label='ML Estimator', color='blue', density=True)

plt.title('Histogram of Squared Errors (ML)')

plt.xlabel('Squared Error')

plt.ylabel('Density')

plt.legend()

plt.subplot(1, 2, 2)

plt.scatter(true_signals, ml_estimates, alpha=0.3, label='ML Estimator', color='blue', s=10)

plt.plot([0, a], [0, a], 'k--', label='Ideal')

plt.title('True Signal vs ML Estimates')

plt.xlabel('True Signal (s)')

plt.ylabel('Estimated Signal')

plt.legend()

plt.tight_layout()

plt.show()

# Pair 2: MAP Estimator - Closed-Form

plt.figure(figsize=(12, 4))

plt.subplot(1, 2, 1)

plt.hist(map_errors_proj, bins=50, alpha=0.7, label='MAP Estimator - Closed-Form', color='green', density=True)

plt.title('Histogram of Squared Errors (MAP - Closed-Form)')

plt.xlabel('Squared Error')

plt.ylabel('Density')

plt.legend()

plt.subplot(1, 2, 2)

plt.scatter(true_signals, map_estimates_closed_form, alpha=0.3, label='MAP Estimator - Closed-Form', color='green', s=10)

plt.plot([0, a], [0, a], 'k--', label='Ideal')

plt.title('True Signal vs MAP Estimates (Closed-Form)')

plt.xlabel('True Signal (s)')

plt.ylabel('Estimated Signal')

plt.legend()

plt.tight_layout()

plt.show()

# Pair 3: MMSE Estimator - Closed-Form

plt.figure(figsize=(12, 4))

plt.subplot(1, 2, 1)

plt.hist(mmse_errors_closed_form, bins=50, alpha=0.7, label='MMSE Estimator - Closed-Form', color='red', density=True)

plt.title('Histogram of Squared Errors (MMSE - Closed-Form)')

plt.xlabel('Squared Error')

plt.ylabel('Density')

plt.legend()

plt.subplot(1, 2, 2)

plt.scatter(true_signals, mmse_estimates_closed, alpha=0.3, label='MMSE Estimator - Closed-Form', color='red', s=10)

plt.plot([0, a], [0, a], 'k--', label='Ideal')

plt.title('True Signal vs MMSE Estimates (Closed-Form)')

plt.xlabel('True Signal (s)')

plt.ylabel('Estimated Signal')

plt.legend()

plt.tight_layout()

plt.show()

# To store y_bar for selected trials

selected_trials = [0, np.random.randint(0, num_trials)] # First, random

selected_y_bars = []

selected_s_true = []

# Simulation Loop

for trial in range(num_trials):

# Randomly choose a true signal s within (0, a)

s = np.random.uniform(0, a)

true_signals[trial] = s

# Generate L observations with Gaussian noise

y = s + np.random.normal(0, sigma, L)

y_bar = np.mean(y)

# ML Estimator

s_ml = y_bar

ml_estimates[trial] = s_ml

# MAP Estimator via Closed-Form

s_map_proj = map_estimator_closed_form(y_bar, a)

map_estimates_closed_form[trial] = s_map_proj

# MAP Estimator via Numerical Root-Finding

s_map_num = map_estimator_numerical(y_bar, L, sigma, a)

map_estimates_numerical[trial] = s_map_num

# MMSE Estimator via Numerical Integration

s_mmse_num = mmse_estimator_numerical(y_bar, L, sigma, a)

mmse_estimates_numerical[trial] = s_mmse_num

# MMSE Estimator via Closed-Form Expression

s_mmse_closed = mmse_estimator_closed_form(y_bar, L, sigma, a)

mmse_estimates_closed[trial] = s_mmse_closed

# Store data for selected trials

if trial in selected_trials:

selected_y_bars.append(y_bar)

selected_s_true.append(s)

# To make the plot readable, especially with huge trials, we'll plot a subset, e.g., every k-th trial.

subset_indices = np.arange(0, num_trials, 10)

subset_trials = subset_indices + 1 # Trial indices starting from 1

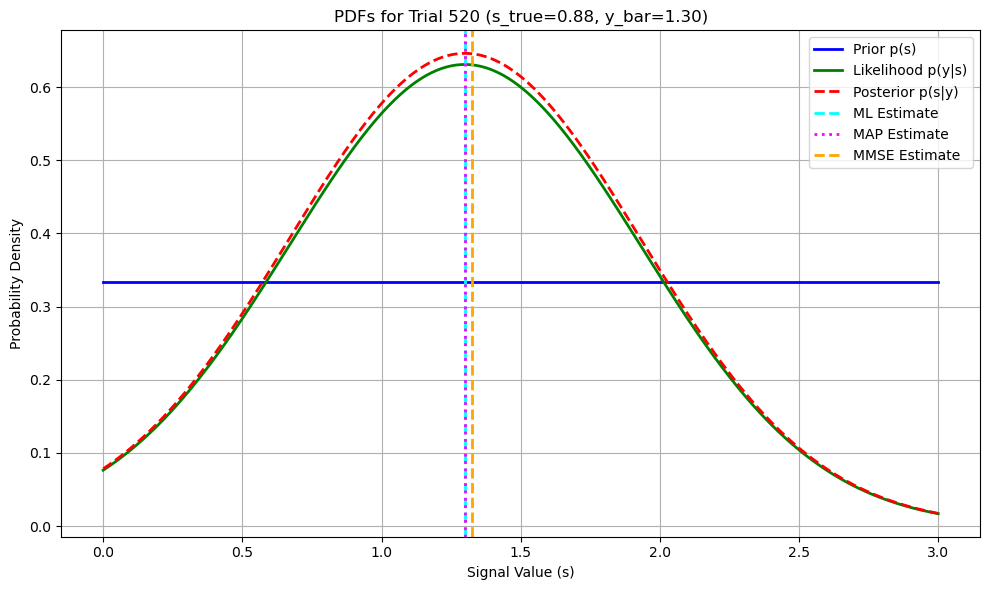

# Plotting PDFs for Selected Trials

for idx, trial in enumerate(selected_trials):

s_true = selected_s_true[idx]

y_bar = selected_y_bars[idx]

# Define s range for plotting

s_values = np.linspace(0, a, 500)

# Prior p(s): Uniform distribution

p_s = np.ones_like(s_values) / a # Uniform on [0,a]

# Likelihood p(y | s): Gaussian centered at y_bar with variance sigma^2 / L

# Since y_bar is the sample mean of L observations, the likelihood of y_bar given s is N(s, sigma^2 / L)

p_y_given_s = norm.pdf(y_bar, loc=s_values, scale=sigma / np.sqrt(L))

# Posterior p(s | y): p(y | s) * p(s) normalized

p_s_given_y = p_y_given_s * p_s

p_s_given_y /= np.trapz(p_s_given_y, s_values) # Normalize

# Estimators

s_ml = ml_estimates[trial]

s_map = map_estimates_closed_form[trial]

s_mmse = mmse_estimates_closed[trial]

# Plotting

plt.figure(figsize=(10, 6))

plt.plot(s_values, p_s, label='Prior p(s)', color='blue', linewidth=2)

plt.plot(s_values, p_y_given_s, label='Likelihood p(y|s)', color='green', linewidth=2, linestyle='-')

plt.plot(s_values, p_s_given_y, label='Posterior p(s|y)', color='red', linewidth=2, linestyle='--')

# Mark estimators on the posterior

plt.axvline(s_ml, color='cyan', linestyle='--', linewidth=2, label='ML Estimate')

plt.axvline(s_map, color='magenta', linestyle=':', linewidth=2, label='MAP Estimate')

plt.axvline(s_mmse, color='orange', linestyle='--', linewidth=2, label='MMSE Estimate')

plt.title(f'PDFs for Trial {trial + 1} (s_true={s_true:.2f}, y_bar={y_bar:.2f})')

plt.xlabel('Signal Value (s)')

plt.ylabel('Probability Density')

plt.legend()

plt.grid(True)

plt.tight_layout()

plt.show()